IF YOUR COLLECTION IS WORLD CLASS, INSURANCE SHOULD NOT BE AN AFTERTHOUGHT

By Debbie Carlson

Collecting sports memorabilia has been a fun pastime for decades and lately, values for all types of sports collectibles have sharply increased.

Like other collectibles, sports memorabilia have benefited from a good U.S. economy, the growth of internet sales and investment interest in real assets. This has increased prices for objects like baseball cards, jerseys and game-used artifacts.

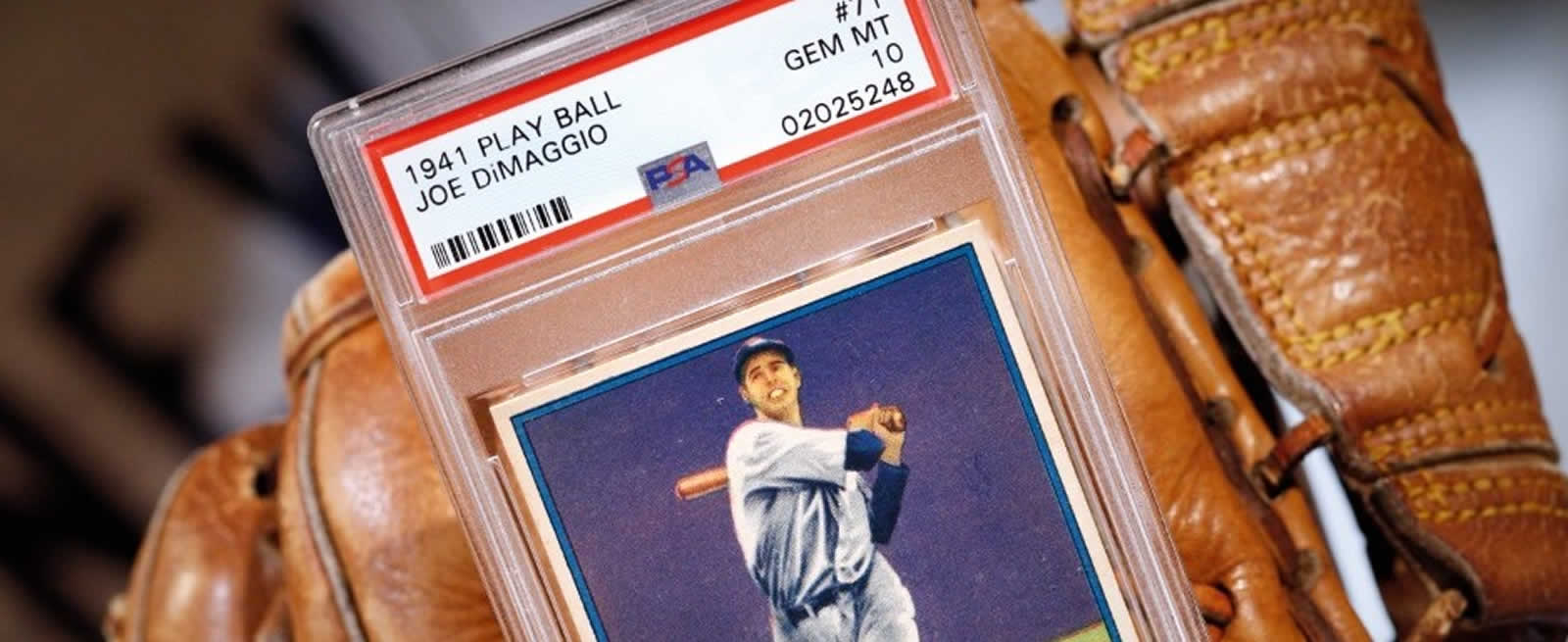

How far are prices going? Last year, a 1937 Lou Gehrig game-worn New York Yankees jersey sold for $2.58 million. A lower-quality grade 1909-11 T206 Honus Wagner tobacco card, often considered one of the most collectible baseball cards, sold privately for $1.2 million. And a 1952 Topps Mickey Mantle #311 card realized $765,000 (see “2019’s Home Runs”).

Granted, not every sports collectible is going to fetch a record-breaking price, but these are examples of the value some collectibles can command. That means whether people collect sports memorabilia for nostalgia, love of the game or as part of an investment portfolio, proper care for these objects takes on added importance, including maintaining adequate insurance levels.

The right insurance

Many sports collectors initially use their homeowner’s insurance coverage to protect their valuables. But homeowner’s insurance often does not cover items like baseball jerseys, cards or other sports memorabilia. James Appleton, director of sales, special risk, at MiniCo Insurance Agency, says generally, homeowner’s insurance provides limited coverage for anything of a collectible nature.

Depending on the homeowner’s policy, if there is a claim, the insurance company may pay a depreciated amount, or cash value, rather than full collectible value, Appleton says. In a worst-case scenario, the insurer might just pay for the cardboard versus the collectible value of what was lost. “There’s usually a happy medium in there obviously, but, like I said, in the extreme case, homeowner’s policies typically are there just to make you whole and it’s generally outside of a full collectible value,” Appleton says.

Even if the current value would fall under a homeowner’s insurance cap, collectors may want to consider a separate policy anyway. “If you have a valuable collection,” says Robert Brodwater, director at Collectibles Insurance Services, “you should consider getting it properly insured.”

“Usually,” adds Erin Bast, a senior underwriter at Huntington T. Block, “we start to see people wanting a separate fine-art policy when, let’s say, they’ve bought that $60,000 jersey or that $70,000 home-run bat that won the World Series.”

Most fine arts and collectibles insurance coverage are blanket policies and cover a greater array of losses, including mysterious circumstances, and offer full collectible value. Collections insurance also has fewer exclusions, say Appleton and Bast. Standard policy exclusions include wear and tear, gradual deterioration and botched restoration. Depending on the policy, it may have a very low or no deductible. Annual policy premiums will depend on the collection’s value, but can cost $500 to $1,000.

When collectors buy a policy, Bast says her firm may ask them a few questions, such as what the collection consists of, how many items, total value, if there’s a particular item that is likely the most valuable and how the collection is protected.

Policyholders often come up with a collection’s value, usually based on a recent appraisal or market value. To ensure coverage levels are adequate, Bast says Huntington T. Block recommends collectors have their items valued every three to five years since the value of sports memorabilia can fluctuate. Appleton says MiniCo, which partners with AXA Art Insurance, doesn’t require proof of value when buying the policy, only when filing a claim, which is when they would need records to verify the insured value.

Taking care of collections

There are several precautions owners of any collection should take, such having a security system and maintaining adequate temperatures where the objects are held.

Sports-memorabilia collections have a few unique needs, says Laura Doyle, vice president, art, jewelry and valuable collections manager at Chubb. Anything that is displayed should be stored in UV-rated protective cases. Textiles and autographs, for example, are susceptible to fading when exposed to sunlight if not protected. Doyle also recommends using archival boxes for smaller items. For sports cards, use archival tissue and/or non-toxic archival plastic sleeves or cases to prevent damage.

Collectors need to be careful where they display and store their items. Avoid areas that are below plumbing lines, and think twice before keeping collections in basements, which are more likely to be susceptible to water damage and dampness.

When applying for a policy, some insurers specifically ask if an owner has a basement, if goods are stored there and if there’s a risk for flooding. Collections stored on the floor or just slightly off the ground when they suffer water damage potentially might not be paid out. “The policy very much requires certain levels of basic caretaking,” Appleton says.

Not storing a collection in a basement might seem intuitive, but that’s not necessarily so. “We tend to see that in many cases, sports memorabilia collections might be displayed in a finished basement,” Doyle says. “And we have had cases where there has been flooding and the client was able to be compensated for that loss because it was covered under their valuables policy.”

In other cases, collectors sometimes travel to sports-memorabilia shows and take their collectibles with them. If that’s the case, Appleton says, as long as the owner keeps the collection within their care, custody and control at all times, the policy should be in force. If collections will be displayed at a gallery or museum, he recommends that owners tell their insurer how long the collection will be out of the owner’s control. Depending on the length of time out of the owner’s possession, the policy may cover the display or the insurer may require the museum to cover it.

DEBBIE CARLSON is a Chicago freelancer whose work has appeared in Barron’s, U.S. News & World Report and The Wall Street Journal.

FAKE? OUT OF LUCK

Key drivers to the value of sports-memorabilia are rarity, condition and provenance. These days, another factor is just as important: authenticity. Insurance won’t reimburse policyholders if the items they own are discovered to be fake.

“It’s really important to do your due diligence when making a purchase,” says Laura Doyle at Chubb. James Appleton at MiniCo Insurance Agency concurs. Before buying an item, research the provenance and uniqueness of the object, along with the seller’s credentials.

It’s becoming harder to detect fakes, so authentication is key. Appleton cites a few tips from AXA Art’s authentication experts on how to detect fraud. Authentication experts, he says, can compare paint pigmentations, signatures and the size of the object to make sure the piece is genuine. Forged signatures are also an issue for sports collectors. To check if a signature was rubber-stamped, look for smudges, distortions and other irregularities.

And watch out for anachronistic irregularities, Appleton says. For example, signatures in ballpoint pen first appeared in 1945 and signatures in black permanent markers appeared after 1964.

Depending on the sport, certain athletes or sports people command a premium, some brands are more popular, and each game has specialized equipment and materials. Certain dates, like when a team won a championship, are key to value. Even if articles are genuine, it’s important to know the trends to assess value, according to AXA Art tips.

Verifying whether an item is the genuine article, Doyle and Appleton say, in the end comes down to the buyer. “We always recommend a third-party professional that specializes in authenticating sports memorabilia,” Appleton says.

Debbie Carlson

This article appears in the Spring/Summer 2020 edition of The Intelligent Collector magazine. Click here to subscribe to the print edition.